Greater Bay Area Residential and CRE Investments to Takeoff Amid Border Reopening

- Written by Daily Sun

- Secondary market home prices remained under pressure, although primary home prices in some cities were lifted due to a focus on high-end projects. Recovery is expected in the GBA housing market along with the mainland-Hong Kong border reopening.

- Total GBA CRE investment volume recorded RMB64.9 billion in 2022, taking an approximately 29% share of the large-size deals (>RMB 100 million) in China, with Shenzhen surpassing Beijing as the second-highest ranked city by investment volume.

- Investment interest in new economy assets such as industrial and logistics facilities and data centres has picked up noticeably, with the rise of China's Real Estate Investment Trusts (C-REITs) also propelling greater investment appetite for industrial parks, biomedical facilities, and logistics assets.

HONG KONG SAR and BOSTON - Media OutReach - 11 January 2023 - Global real estate services firm Cushman & Wakefield today published its Greater Bay Area Residential and Investment Market 2022 Review and 2023 Outlook. The GBA's residential market slowed noticeably in 2022 in the wake of the pandemic, with overall transaction numbers and secondary home prices both dropping. In contrast, transactions in the CRE market held up well. The relaxation of quarantine measures in the mainland, coupled with the border reopening, should bring greater positivity to overall market sentiment in 2023, and support a pick-up in transactions in both residential and CRE investment markets.

GBA Residential Sales Volume and Price

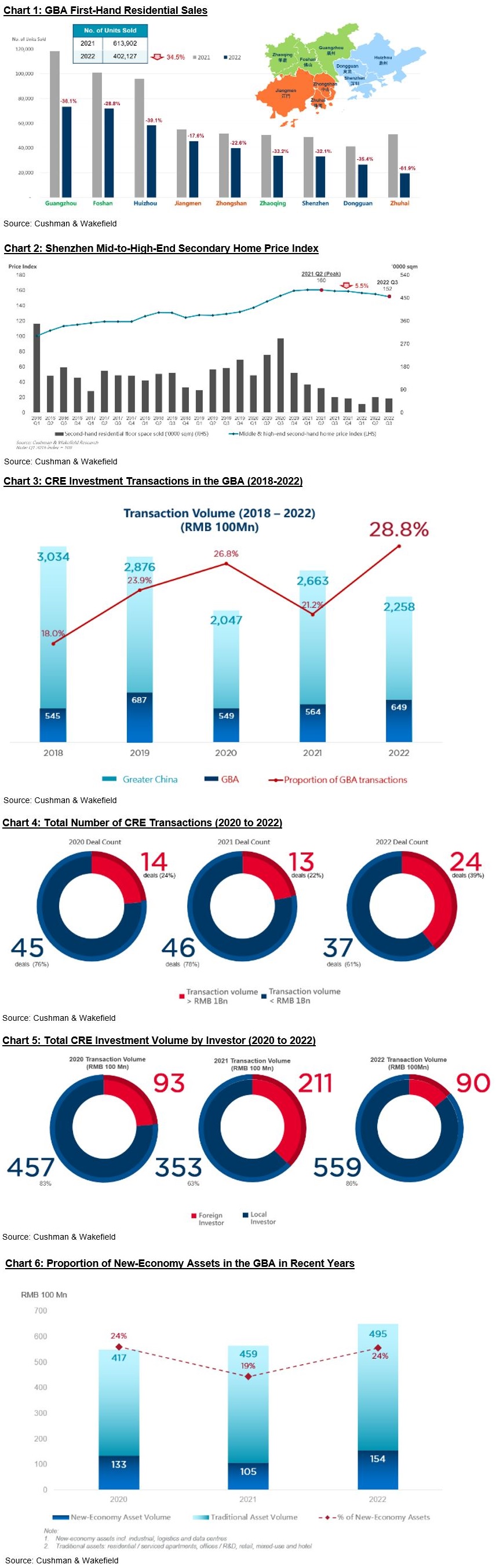

Impacted by the pandemic and dampened economic growth, GBA residential transactions dropped noticeably in 2022, with primary market sales recorded at around 400,000 units, down by approximately 35% y-o-y (Chart 1). Among the city markets, Zhuhai, one of the most popular locations for Hong Kong buyers, saw the most notable drop, partially due to the travel restrictions that have slowed potential purchases from across the border.

Alva To, Cushman & Wakefield's Vice President, Greater China & Head of Consulting, Greater China said, "Despite the overall slowdown of GBA residential transactions in 2022, the central government has recently relaxed national pandemic policies and border restrictions with Hong Kong, which will likely help drive residential purchases in 2023. Initially, Hong Kong buyers may go over the border to finalize their previously on-hold transactions, which may not trigger an immediate V-shape recovery, yet we believe market momentum will pick up towards 2H 2023, with transaction volume expected to rise by 20-25% in 2023."

As for residential prices, first-hand market home values picked up in some GBA cities as most purchases were concentrated on high-end properties, despite limited transaction activities. However, in terms of secondary market homes, prices have fallen by more than 5% from the 2021 peak, even in leading cities such as Shenzhen, according to Cushman & Wakefield research data (Chart 2). Looking into 2023, residential prices are expected to regain stability as price corrections should further narrow amid the relaxation of pandemic rules.

GBA CRE Investment Transaction Number and Value

Despite the impact of the pandemic, CRE investment in the GBA was relatively active in 2022, with more large-sized deals (>RMB 100 million) taking place in 2H 2022, bringing the full year record to RMB64.9 billion. This volume accounted for around 29% of the nation's total transactions, the highest proportion since 2018 (Chart 3). Shenzhen and Guangzhou were most active among all GBA cities, with Shenzhen recording 40 CRE investment deals totalling RMB44.2 billion in 2022, surpassing Beijing and becoming the second-highest ranked city by CRE investment consideration in mainland China. Meanwhile, Guangzhou also recorded 19 deals, totalling RMB19.9 billion.

By Transaction Value and Capital Source

The full-year of 2022 recorded 24 CRE investment transactions at over RMB1 billion, accounting for approximately 40% by market share in the GBA, significantly higher than that in 2020 and 2021. The balance of 37 transactions were at less than RMB1 billion (Chart 4). As for the investor origin, transaction volume by domestic investors jumped by more than 50% y-o-y to reach RMB55.9 billion, accounting for an 86% share of the market. This reflects the fact that local capital has been largely supporting market activity, with some deals also involving receivership transactions. In contrast, foreign capital was relatively muted, accounting for merely 14% of the market. We believe the foreign investment market share in 2023 could potentially rebound to around 35% and return to the 2021 level, as the mainland fully opens up to the rest of the world.

GBA CRE Investment by Asset Types

Office and R&D office properties remain the most popular sector and dominated the GBA investment market in 2022, accounting for more than half of the total CRE investment volume in the year. Charli Chan, Cushman & Wakefield's Executive Director, Capital Markets, China shared, "Office assets in the GBA are still sought after by the market, although in 2022 buyers largely acquired for self-use purposes, accounting for 70% of office transactions. With the relaxation of the mainland's border and pandemic policies, traditional sectors such as office and retail are expected to pick up in 2H 2023. In addition, investment in new economy assets, such as industrial parks, logistics, and data centres, also grew in 2022 to reach RMB15.4 billion, accounting for 24% of the total volume."

Charli Chan concluded, "Since June 2021, the central government has been actively promoting the development of C-REITs, aiming to stimulate foreign investment while providing real estate firms with more financing channels. The market has recorded at least 13 deals related to C-REITs in 2022. The rapid development of C-REITs, coupled with policy support, has prompted interest in industrial parks, biomedical facilities, logistics, and rental apartments. We expect these property types to stay attractive in 2023, bringing a more fruitful year for transactions, while real estate funds are expected to renew their activity levels."

Photo caption:

Charli Chan, Cushman & Wakefield's Executive Director, Capital Markets, China (Left) and Alva To, Cushman & Wakefield's Vice President, Greater China & Head of Consulting, Greater China shared Greater Bay Area Residential and Investment Market 2022 Review and 2023 Outlook in today's press conference.

Please click here to download photos.

Hashtag: #CushmanWakefield

The issuer is solely responsible for the content of this announcement.

About Cushman & Wakefield

Cushman & Wakefield (NYSE: CWK) is a leading global real estate services firm that delivers exceptional value for real estate occupiers and owners. Cushman & Wakefield is among the largest real estate services firms with approximately 50,000 employees in over 400 offices and 60 countries. Across Greater China, 23 offices are servicing the local market. The company won four of the top awards in the Euromoney Survey 2017, 2018 and 2020 in the categories of Overall, Agency Letting/Sales, Valuation and Research in China. In 2021, the firm had revenue of $9.4 billion across core services of property, facilities and project management, leasing, capital markets, valuation, and other services. To learn more, visit www.cushmanwakefield.com.hk or follow us on LinkedIn ( https://www.linkedin.com/company/cushman-&-wakefield-greater-china).